| Card |

|---|

| default | true |

|---|

| id | 1 |

|---|

| label | Financial Concepts |

|---|

| Buyer It is a financing agreement for payment of inputs or services purchased by the customer from their suppliers. It is aimed at companies that seek to buy in cash from their suppliers, however, with a longer term and better rates, as well as negotiating payment with the bank under conditions appropriate to their cash flow. Guarantees: trade notes, checks, collateral and debtor liable. Advantages for the buyer/borrower: - Enables the replacement of supplier financing for banking financing when the bank offers more attractive interest rates.

- Possibility of negotiating with the seller the benefits they obtain; similar to those of the seller.

- Flexibility for cash flow planning.

- Improved operational results: reduced interest at purchase price.

- Competitive Advantage compared to its players that do not use the product.

Vendor It is a sales financing agreement based on credit assignment, which allows a company to sell its product in installments to legal entities and receive in cash. The Vendor assumes the buyer company is a regular customer of the seller, since the seller takes the risk of the business with the bank. Possibility of using electronic means to contract operations. Guarantees: Supplier and seller guarantee. Advantages for the supplier/seller: - Cash advance: payment up front.

- Tax charge reduction, as sales are effected in cash.

- More flexible financing terms.

- Interest Rate Flexibility

- More competition and better financial efficiency.

- Longer payment term for the purchaser.

- Faster turnover of goods.

|

| Card |

|---|

| default | true |

|---|

| id | 2 |

|---|

| label | Financial Processes |

|---|

| | Accounts Payable |

|---|

Control of bills payable. Budget control by class, in up to 5 different currencies. Posting of bills payable - Manual.

- By Lot.

- Automatically.

Ease and speed in dealings between the company and the bank: - Automatic payment by bank.

- Check issuance and control in continuous or single form

- Banking communication (CNAB standard).

- Control of bank balances.

- Issue of bank statements.

- Issue of payment bordereau.

Follow-up of Supplier history: - Highest balance due.

- Average arrears period.

- Maximum arrears period.

- Current Account Ledger.

Control of balance payable: - Total amount due.

- Total amount falling due.

- Number of outstanding bills.

- Number of bills overdue.

- Ledger.

Accounting of transactions: on-line and off-line. Control of company cash (balance). |

| Accounts Receivable |

|---|

Includes the following criteria: Control of bills receivable. Advances. Provisional bills. Budget control by class, in up to 5 different currencies Investment control Financial agreement control. Ease and speed in dealings between the company and the bank: Automatic bordereau. Bank instructions Banking communication (CNAB standard): - From company to Bank.

- From Bank to company.

Bank balances. Issue of statements. Bank reconciliation. Bank bills. CNAB checking reports. Commission Control: - Commissions by issue of bills.

- Commissions by positing bills (with different percentages)

Monitoring of customer history: - Highest balance due.

- Average arrears period.

- Maximum arrears period.

- Bills protested.

- Payments made.

- Current Account Ledger.

Control of customer balance: - Overdue.

- Falling due.

- Orders without credit.

- Orders with credit.

Control of balances receivable: - Total amount due.

- Total amount falling due.

- Number of outstanding bills.

- Number of bills overdue.

- Auxiliary ledger.

- Collection summary.

- Accounting of transactions: on-line and off-line.

Financial projection in 4 currencies: - By reference (in days).

- By inflationary trend.

- Control of availability (by cash)

|

| Cash Flow |

|---|

It is a very efficient management tool that includes the set of income and disbursements of financial resources by the company in a given period. The analysis and control of information facilitates decision making according to the following criteria: - Survey of the funds required for executing the company's action plans.

- Use, in the best possible way, the available or exceeding resources, preventing them from being idle and being directed to the best applications.

- Planning and control resulting from sales, production and operating expenses projections, as well as data related to activity indexes, average period of inventory rotation, amounts receivable and payable.

- Settle the company's liabilities on the due date.

- Analyze the credit sources that offer less burdensome loans, if the company needs funds.

- Enable coordination among the resources that will be allocated in current assets, sales, investments and debts.

- Consolidation of accounts payable and receivable

- Control in 5 currencies

- Financial simulation considering hypothetical entry of loans, advances or deferrals

- Consideration, in addition to bills, of purchase and sales orders in portfolio, future investments/redemptions, commissions, bills in arrears and interim bills;

- Graphical representation of cash flow.

- Daily segregation of bills.

| Informações |

|---|

| Petty Cash It allows the control of the amounts available for immediate and small expenses in order to manage the flow of money in and out in an agile, simple and less bureaucratic way. This control is made according to the following options: - Maintenance.

- Transactions.

- Recalculation.

|

APV - Adjustment at Present Value The AVP makes the adjustment to demonstrate the present value of a future cash flow that may be represented by inflows or outflows of funds (or an equivalent amount; for example, credits that decrease future outflows would be equivalent to inflows of funds). To determine the present value of cash flow, the following information is required: value of the future flow (considering all terms and conditions of the contract), date of the financial flow, and discount rate applicable to the transaction. To make the determination of CPC 12 (Accounting Pronouncements Committee) feasible, the Financial module has the following features: - Only offline calculation of APV concerning bills of portfolio payable and receivable.

- Processing wizard to help parameterization and application of discount rates in selected bills.

- Parameterization of calculation and respective accounting through multiple thread processes.

- Multiple calculations in the same period, differentiated by portfolio and selection criteria.

- Execution for retroactive periods, considering posting events and the respective accomplishments.

- Definition of the reversal of adjustment processing made by the process selection.

- Definition of the adjustment value of a bill through a formula previously registered in the Formula register of ERP (SM4).

- Simulation of the constitution of bill adjustment, enabling evaluation to start or not the process of portfolio allocation.

The following routines comprise the process of APV calculation: - Financial Indexes.

- Index Update.

- APV Accounts Receivable Calculation.

- APV Accounts Payable Calculation.

- APV Accounts Receivable Check.

- APV Accounts Receivable Bills.

- APV Accounts Payable Check.

- APV Accounts Payable Bills.

| Bank Balance in Multiple Currencies |

|---|

This resource controls checking accounts in currencies other than the current one (BRL). Thus, if the company has checking accounts abroad, transactions can be controlled in other currencies (for example: USD, EUR). To use this functionality, it is necessary to register the information in the Banks routine and fill in the Currency field, consequently, the bank balance in multiple currencies is enabled to be used in the following routines: - Accounts Receivable.

- Accounts Payable.

- Transfers.

- Posts Receivable.

- Posts Payable.

- Bank Transaction.

- Automatic Posts Receivable.

- Payment Bordereau.

|

| Card |

|---|

| The Microsiga Protheus® system has the bookkeeping feature for the Financial module that allows the exchange of standardized and pre-established information by Banks through electronic files. This process guarantees more reliability, speed in data processing and elimination of manual controls. CNAB (National Council for Bank Automation) establishes the rules to format files through specific guidelines. First, the system administrator must configure the remittance and return files for the bills in the Configurator module: | Model 1 | Remittance | Return |

|---|

| CNAB Receivable | In the Configurator module, access the CNAB Receivable option, and configure the remittance file of Accounts Receivable according to the provisions and rules described in the Bank guideline. In the Financial module, access the Bank Parameters option and register the information. Note: In the EE_Tabela field, enter the code of the relationship table between the bill type in Financial and the bill type in the bank. The system default is Table 17 of the Configurator environment. However, it is possible to generate new tables to perform the same treatment. In the Configurator module, access the Tables option and check which table is used for this Bank (through the Bank Parameters Register). If it is Table 17, check the bank return standard regarding the bill type and update the table in the Configurator module. Example: Considering that, for NF type bills, the bank identifies as 01, Table 17 is as follows: Thus, the System identifies the NF type bills of the System as equivalent to the bills that the bank identifies as 01. In the Financial module, go to the CNAB Occurrences option and register the Bank occurrences to submit Accounts Receivable. In the Financial module, access the Bordereau option and generate the bordereaux with the bills to be sent to the Bank. In the Financial module, access the Generate File Receivable option and generate the text file to be sent to the Bank. | In the Configurator module, access the CNAB Receivable option and set the return file of Accounts Receivable according to the provisions and rules described in the Bank guideline. The system generates a standard layout of the return file while adding this routine. The file rows must not be changed. You only need to enter the columns of Initial and Final Positions. In the Financial module, access the Bank Parameters option and register the information. Note: In the EE_Tabela field, enter the code of the relationship table between the bill type in Financial and the bill type in the Bank. The system default is Table 17 of the Configurator environment. However, it is possible to generate new tables to perform the same treatment. If the Bank Parameter register is already configured, you do not have to add a record again, except if you need to work with two tables of type identification in the system, send/receive. In the Configurator module, access the Tables option and check which table is used for this Bank (through the Bank Parameters Register). If it is Table 17, check the bank return standard regarding the bill type and update the table in the Configurator module. Example: Considering that, for NF type bills, the bank identifies as 01, Table 17 is as follows: Thus, the System identifies the NF type bills of the System as equivalent to the bills that the bank identifies as 01. In the Financial module, access the CNAB Occurrences option and register the Bank occurrences for the return of Accounts Receivable. Accounting of posts of accounts receivable uses the standard entry from 521 to 526 for posting, 527 for cancellation, and 562 for bank expenses accounting. In the Financial module, access the CNAB Return Report option and check whether bills are received correctly, because a list of divergences between the bank return text file and the system bill file is displayed in it. In the Financial module, access the CNAB Receivable Return option and receive the bank return text file, according to the parameters defined.

| | CNAB Payable | In the Configurator module, access the CNAB Payable option and configure the return file of Accounts Payable according to the provisions and rules described in the Bank guideline. In the Financial module, access the Bank Parameters option and register the information. Note: in the E5_Tabela field, enter the code of the relationship table between the bill type in Financial and the bill type in the bank. The system default is Table 17 of the Configurator module. However, it is possible to generate new tables to perform the same treatment. In the Configurator module, access the Tables option and check which table is used for this Bank (through the Bank Parameters register). If it is Table 17, check the bank return standard regarding the bill type and update the table in the Configurator module. Example: Considering that, for NF type bills, the Bank identifies as 01, Table 17 is as follows: Thus, the System identifies the NF type bills of the System as equivalent to the bills that the bank identifies as 01. You do not need to register occurrence for Submission of CNAB Payable. In the Financial module, access the Bordereau option and generate the payment bordereaux with the bills to be sent to the Bank. In the Financial module, access the Generate File Payable option and generate the text file to be sent to the Bank. | In the Configurator module, access the CNAB Payable option and configure the return file of Accounts Payable according to the provisions and rules described in the Bank guideline. The system generates a standard layout of the return file while adding this routine. The file rows must not be changed. You only need to enter the columns of Initial and Final Positions. In the Financial module, access the Bank Parameters option and register the information. Note: in the EE_Tabela field, enter the code of the relationship table between the bill type in Financial and the bill type in the Bank. The system default is Table 17 of the Configurator module. However, it is possible to generate new tables to perform the same treatment. If the Bank Parameter register is already configured, you do not have to add a record again, except if you need to work with two tables of type identification in the system, send/receive. In the Configurator module, access the Tables option and check which table is used for this Bank (through the Bank Parameters register). If it is Table 17, check the bank return standard regarding the bill type and update the table in the Configurator module. Example: Considering that, for NF type bills the Bank identifies as 01, Table 17 is as follows: Thus, the System identifies the NF type bills of the System as equivalent to the bills that the bank identifies as 01. In the Financial module, access the CNAB Occurrences option and register the Bank occurrences for the return of Accounts Receivable. Accounting of posting accounts payable uses the standard entry 530 for Posting and 531 for Cancellation. In the Financial module, access the CNAB Return Report option and check whether bills are received correctly, because a list of divergences between the bank return text file and the system bill file is displayed in it. In the Financial module, access the CNAB Receivable Return option and receive the bank return text file, according to the parameters defined.

|

| Model 2 | Remittance | Return |

|---|

| CNAB Receivable | In the Configurator module, access the CNAB Model 2 option and configure the remittance file. In the Financial module, access the Bank Parameters option and register the information. Note: In the EE_Tabela field, enter the code of the relationship table between the bill type in Financial and the bill type in the bank. The system default is Table 17 of the Configurator module. However, it is possible to generate new tables to perform the same treatment. In the Configurator module, access the Tables option and check which table is used for this Bank (through the Bank Parameters register). If it is Table 17, check the bank return standard regarding the bill type and update the table in the Configurator module. Example: Considering that, for NF type bills, the bank identifies as 01, Table 17 is as follows: Thus, the System identifies the NF type bills of the System as equivalent to the bills that the bank identifies as 01. In the Financial module, go to the CNAB Occurrences option and register the Bank occurrences to submit Accounts Receivable. In the Financial module, access the Bordereau option and generate the bordereaux with the bills to be sent to the Bank. In the Financial module, access the Generate File Receivable option and generate the text file to be sent to the Bank. | In the Configurator module, access the CNAB Model 2 option and configure the return file. In the Financial module, access the Bank Parameters option and register the information. Note: In the EE_Tabela field, enter the code of the relationship table between the bill type in Financial and the bill type in the Bank. The system default is Table 17 of the Configurator module. However, it is possible to generate new tables to perform the same treatment. In the Configurator module, access the Tables option and check which table is used for this Bank (through the Bank Parameters register). If it is Table 17, check the Bank return standard regarding the bill type and update the table in the Configurator module. Example: Considering that, for NF type bills, the bank identifies as 01, Table 17 is as follows: Thus, the System identifies the NF type bills of the System as equivalent to the bills that the bank identifies as 01. In the Financial module, access the CNAB Occurrences option, register the Bank occurrences for the return of Accounts Receivable. Accounting of posts of accounts receivable uses the standard entry from 521 to 526 for posting, 527 for cancellation, and 562 for bank expenses accounting. In the Financial module, access the CNAB Return Report option and check whether bills are received correctly, because a list of divergences between the bank return text file and the system bill file is displayed in it. In the Financial module, access the CNAB Receivable Return option and receive the bank return text file, according to the parameters defined. | | CNAB Payable | In the Configurator module, access the CNAB Model 2 option and configure the remittance file. In the Financial module, access the Bank Parameters option and register the information. Note: in the EE_Tabela field, enter the code of the relationship table between the bill type in Financial and the bill type in the Bank. The system default is Table 17 of the Configurator module. However, it is possible to generate new tables to perform the same treatment. In the Configurator module, access the Tables option and check which table is used for this Bank (through the Bank Parameters register). If it is Table 17, check the Bank return standard regarding the bill type and update the table in the Configurator module. Example: Considering that, for NF type bills, the bank identifies as 01, Table 17 is as follows: Thus, the System identifies the NF type bills of the System as equivalent to the bills that the bank identifies as 01. In the Financial module, access the Payment Bordereau option and generate the bordereaux with the bills to be sent to the Bank. In the Financial module, access the Generate File Payable option and generate the text file to be sent to the Bank. | In the Configurator module, access the CNAB Model 2 option and configure the return file. In the Financial module, access the Bank Parameters option and register the information. Note: In the EE_Tabela field, enter the code of the relationship table between the bill type in Financial and the bill type in the Bank. The system default is Table 17 of the Configurator module. However, it is possible to generate new tables to perform the same treatment. In the Configurator module, access the Tables option and check which table is used for this Bank (through the Bank Parameters register). If it is Table 17, check the Bank return standard regarding the bill type and update the table in the Configurator module. Example: Considering that, for NF type bills, the bank identifies as 01, Table 17 is as follows: Thus, the System identifies the NF type bills of the System as equivalent to the bills that the bank identifies as 01. In the Financial module, go to the CNAB Occurrences option and register the Bank occurrences to submit Accounts Receivable. Accounting of posting accounts payable uses the standard entry 530 for Posting and 531 for Cancellation. In the Financial module, access the CNAB Return Report option and check whether bills are received correctly, because a list of divergences between the bank return text file and the system bill file is displayed in it. In the Financial module, access the CNAB Receivable Return option and receive the bank return text file, according to the parameters defined. |

| Card |

|---|

| default | true |

|---|

| id | 4 |

|---|

| label | Interest |

|---|

| It is the payment of an invested or loaned capital or, even, the ‘rent’ that is paid or charged for the use of the money. It is also the difference between the amount redeemed in a financial investment and its initial value. In any monetarist economy, the cost of lending or borrowing any amount must be measured by means of an index between the price of this credit and its value over a given period of time. This is called the interest rate, which, in turn, is used as a measure to assess both the rate of return on capital from those who have resources and those who do not (loan). In the first case, it is necessary to consider the risk factors, expenses, inflation and a gain one hopes to obtain when applying that rate (so, the higher the better). For the other context, the lower the better. Amount is the term used to classify the initial capital added to the interest of the period. | Simple Interest |

|---|

It occurs when the interest rate always affects the initial capital. The rate, therefore, is called proportional, since it varies linearly over time. In this case, 1% per day reaches 30% per month, which represents 360% per year and so on. Consider the initial capital P applied at simple interest of rate i per period, for n periods. Take into account that simple interest refers to initial capital, so we have the following formula: J = P*i*n J = Interest after nperiods of capital P applied at an interest rate per period equal to i. At the end of n periods, it is clear that the capital is equal to the initial capital added to the interest earned in the period. The initial capital added to interest from the period is called amount (M). Therefore, the formula would be represented as follows: M = P + J J = P + P * i * n M = P + P * i * n So, M = P(1 + i * n)

Example: In the amount of $3,000.00, an interest rate of 5% is applied every month, for five years. Calculate the amount and interest by the end of the period. P = 3,000.00, i = 5% = 5/100 = 0.05 and n = 5 years = 5,12 = 60 months. J = 3,000.00 * 0.05 * 60 = 9,000.00. M = 3000(1 + 0.05*60) = 3,000(1+3) = 12,000.00. |

| Compound Interest |

|---|

Occurs when the interest rate is levied on the initial capital, plus accrued interest up to the previous period. The rate varies exponentially over time and, in this case, 1% per day is not equal to 30% per month, which in turn, will not be 360% per year. The use of compound interest is very common in the financial system and, therefore, more useful for calculating everyday problems. The interest generated for each period is added to the main to calculate interest for the following period. Capitalization is when interest is incorporated into the main, so, after three months of capitalization, for example, it is possible to notice the following scenario: First month: M =P.(1 + i) Second month: the main is equivalent to the previous month: M = P x (1 + i) x (1 + i). Third month: the main is equivalent to the previous month: M = P x (1 + i) x (1 + i) x (1 + i). This context results in the formula: M = P(1 + i)n The rate i must be expressed in the same time measurement of n, which means that both must be in the same unit, that is, interest rate per year for n years. In the system, the rate entered is processed as annual rate. Thus, n must be converted into years, that is, 1 month is equal to 1/12 or 30/360, so time is in the same unit as the interest rate. To calculate interest, decrease the main from the amount at the end of the period: J = M – P Example: In the amount of $6,000.00, an interest rate of 3.5% is applied every month, for one year. P = BRL 6,000.00 n = 1 year = 12 months i = 3.5 % per month = 0.035 M = ? Applying the formula: M = P (1 + i) n M = 6,000 (1 + 0.035)12 M = 6,000 x 1.511 = 9,066.41 |

| Relation between interest and progression |

|---|

In capitalization of simple interest, balance grows in arithmetic progression. In capitalization of compound interest, balance grows in geometric progression. Consider the initial balance of $1,000.00 and an interest rate of 50% in the period. Simple interest: | Period | Balance |

|---|

| 1 | 1,500.00 | | 2 | 2,000.00 | | 3 | 2,500.00 | | 4 | 3,000.00 | | 5 | 3,500.00 | | 6 | 4,000.00 | | 7 | 4,500.00 | | 8 | 5,000.00 | | 9 | 5,500.00 | | 10 | 6,000.00 |

Image Added Image Added

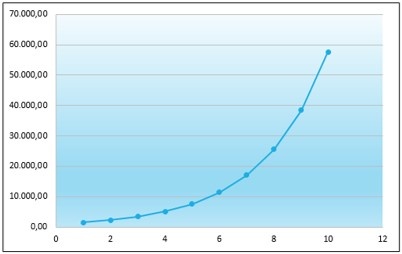

Compound Interest: | Period | Balance |

|---|

| 1 | 1,500.00 | | 2 | 2,250.00 | | 3 | 3,375.00 | | 4 | 5,062.50 | | 5 | 7,593.75 | | 6 | 11,390.63 | | 7 | 17,085.94 | | 8 | 25,628.91 | | 9 | 38,443.36 | | 10 | 57,665.04 |

Image Added Image Added

When calculating compound interest, as it is a geometric progression, interest is charged on interest and it is not possible to divide an annual rate to obtain the daily rate. In this case, use the equivalent rate: i q = (1 + i t)q/t-1 i q = rate for the intended period. i t = rate for the given period. q = intended period. t = given period. p.a. = per annum p.d. = per day. Example: 9.7% p.a. equivalent to: i q = (1 + 0.097) 1/360 - 1 = 0.000257197 iq= 0.02572% (with 5 significant digits) which means: 9.7% p.a. equivalent to 0.02572% per day For compound interest: FV= Future Value PV = Current Value I = Rate (*) n = Period (*)

| Informações |

|---|

| (*) both variables must be in the same time period. |

So: FV = 14,500 (1 + 0.097) 1/360 = 14,503.73 J = 14,503.73 – 14,500.00 = 3.73 Note: 1/360 = 1day in one year. Or using the daily equivalent rate: FV = 14,500 (1 + 0.000257197) 1 = 14,503.73 J = 14,503.73 – 14,500.00 = 3.73 |

|

|

|

|

|